Inflation in IB Economics: Causes, Effects and Why Rising Prices Matter

A clear IB Economics explanation of inflation, including how it is measured, demand-pull inflation, cost-push inflation, effects and policy responses.

Inflation in IB Economics: Causes, Effects and Why Rising Prices Matter

Inflation is one of the most important macroeconomic topics in IB Economics. It affects households, firms, workers, savers, borrowers, governments and international competitiveness.

At a basic level, inflation means prices are rising. More precisely, it is a sustained increase in the general price level of an economy over time. This means inflation is not just one product becoming more expensive. It refers to an overall rise in average prices across the economy.

Inflation matters because it changes the purchasing power of money. If prices rise faster than income, people can buy fewer goods and services. If inflation becomes unstable, firms may find it harder to plan, workers may demand higher wages, and governments or central banks may need to use policy to reduce inflationary pressure.

What inflation means

Inflation is a sustained increase in the general price level. The general price level is the average level of prices across an economy, usually measured using a price index.

A price index tracks the cost of a basket of goods and services over time. This basket may include food, housing, transport, energy, clothing, healthcare, education and other common household expenses. If the cost of the basket rises, the price index rises.

The inflation rate measures the percentage change in the price index over a period of time, usually one year.

For example, if the consumer price index rises from 100 to 105, the inflation rate is 5 percent. This means the average price level has increased by 5 percent.

Inflation is different from a one-time price increase. If oil prices rise once and then stay constant, this may raise the price level, but it is not continuing inflation unless prices keep rising over time.

Inflation is also different from high prices. A country can have high prices but low inflation if prices are stable. Inflation is about the rate of change in prices, not simply the level of prices.

This topic connects directly to macroeconomic objectives, where low and stable inflation is one of the major goals of economic policy.

Why inflation reduces purchasing power

Purchasing power means the amount of goods and services money can buy. When inflation occurs, each unit of money buys less than before.

Suppose a student has $20. If a meal costs $10, the student can buy two meals. If inflation raises the price of the meal to $12.50, the same $20 now buys only 1.6 meals. The nominal amount of money has not changed, but its real value has fallen.

This is why economists distinguish between nominal and real values. Nominal values are measured in current money terms. Real values are adjusted for inflation.

For example, if wages rise by 3 percent but prices rise by 6 percent, nominal wages have increased, but real wages have fallen. Workers receive more money, but their purchasing power is lower.

This distinction is important in IB Economics because students should not assume that higher nominal income means higher living standards. What matters for purchasing power is whether income rises faster or slower than inflation.

Demand-pull inflation

Demand-pull inflation occurs when aggregate demand increases faster than the economy’s ability to produce goods and services. In simple terms, there is too much spending chasing too few goods.

Aggregate demand is total spending in the economy. It includes consumption, investment, government spending and net exports. If households spend more, firms invest more, governments increase spending, or exports rise, aggregate demand may increase.

In an AD/AS diagram, the vertical axis shows the average price level and the horizontal axis shows real output. Demand-pull inflation is shown by a rightward shift of the aggregate demand curve. Short-run aggregate supply stays fixed.

As aggregate demand shifts right, real output increases and the average price level rises. If the economy is close to full employment, the increase in real output may be small, while the increase in the price level may be large. This is because firms struggle to increase output when resources are already heavily used.

Demand-pull inflation is often associated with economic booms, expansionary fiscal policy, low interest rates, rising consumer confidence or strong export demand.

You can study the model behind this in aggregate demand and supply.

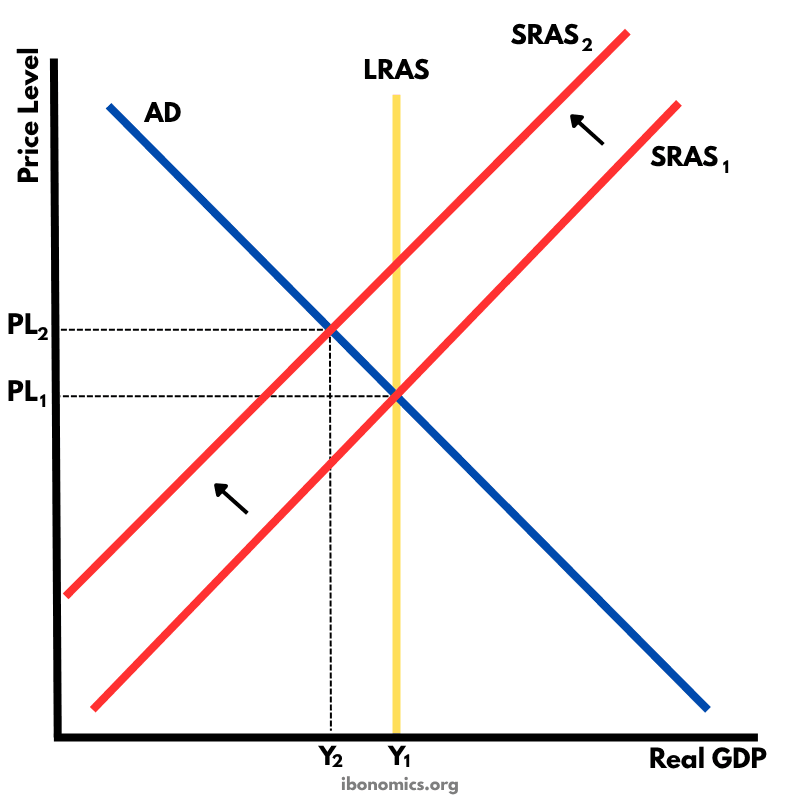

Cost-push inflation

Cost-push inflation occurs when firms face higher costs of production and pass these costs on to consumers through higher prices.

Common causes include higher wages, rising energy prices, more expensive raw materials, supply chain disruptions, higher indirect taxes or a depreciation that makes imported inputs more expensive.

In an AD/AS diagram, the vertical axis shows the average price level and the horizontal axis shows real output. Cost-push inflation is shown by a leftward shift of the short-run aggregate supply curve. Aggregate demand stays fixed.

As short-run aggregate supply shifts left, the average price level rises and real output falls. This creates a difficult situation because inflation rises while output decreases. Unemployment may also increase as firms produce less.

This combination of rising inflation and falling output is sometimes called stagflation.

Cost-push inflation is harder for policymakers to manage than demand-pull inflation. Reducing aggregate demand may lower inflation, but it can also worsen unemployment and reduce output further.

Built-in inflation and expectations

Inflation can also become built into the economy through expectations. If workers expect prices to rise, they may demand higher wages to protect their real income. If firms expect costs to rise, they may raise prices in advance.

This can create a wage-price spiral. Higher prices lead workers to demand higher wages. Higher wages increase firms’ costs. Firms then raise prices again, leading to further wage demands.

Expectations matter because inflation is partly psychological. If people believe inflation will remain high, their behaviour can make inflation more persistent.

Central banks therefore often try to keep inflation expectations stable. If households, firms and workers trust that inflation will stay low and predictable, wage bargaining and pricing decisions may be less inflationary.

This is one reason why credibility is important in monetary policy.

Measuring inflation and its limitations

Inflation is commonly measured using a consumer price index. This tracks changes in the cost of a representative basket of goods and services.

However, measuring inflation is not perfect. Different households buy different goods, so the official inflation rate may not match every person’s experience. A student, a pensioner and a family with children may face different spending patterns.

There can also be quality changes. If a laptop becomes more expensive but also becomes much faster, it is difficult to measure how much of the price increase reflects inflation and how much reflects improved quality.

Substitution can also be a problem. If the price of one good rises, consumers may switch to cheaper alternatives. A fixed basket may not fully capture these changes in behaviour.

Inflation statistics are still useful, but IB students should recognise their limitations. They are estimates of average price changes, not perfect measures of every household’s cost of living.

This connects to the wider issue of measuring economic activity, where economic indicators are useful but limited.

Effects of inflation on consumers

Inflation affects consumers mainly through purchasing power. If incomes do not rise as fast as prices, real income falls. Consumers can afford fewer goods and services, reducing living standards.

Inflation can be especially harmful for people on fixed incomes. Pensioners, students, benefit recipients or workers with wages that adjust slowly may struggle when prices rise quickly.

Inflation can also reduce consumer confidence. If households expect prices to keep rising, they may bring purchases forward, reduce saving or become more cautious depending on the situation.

However, mild inflation is not always harmful. Low and stable inflation may be consistent with economic growth. The problem is usually high, unpredictable or accelerating inflation because it makes planning more difficult and creates uncertainty.

The distributional effects of inflation connect to inequality and poverty, since inflation can affect low-income households more severely if essential goods take up a large share of their spending.

Effects of inflation on firms

Inflation affects firms through costs, prices, planning and competitiveness.

If firms face higher input costs, profit margins may fall unless they can raise prices. Firms with strong pricing power may pass costs on to consumers. Firms in competitive markets may struggle to do this.

High inflation also creates uncertainty. Firms may find it harder to predict future costs, revenues and profits. This can reduce investment because businesses may delay expansion until conditions are more stable.

Inflation can also create menu costs. These are the costs of changing prices, updating catalogues, adjusting systems or communicating new prices to customers.

If domestic inflation is higher than inflation in trading partners, exports may become less competitive. Foreign consumers may switch to cheaper alternatives from other countries. This can reduce export revenue and affect aggregate demand.

Effects of inflation on savers, borrowers and lenders

Inflation redistributes purchasing power between savers, borrowers and lenders.

Savers may lose if the interest rate on savings is lower than the inflation rate. For example, if a savings account pays 2 percent interest but inflation is 6 percent, the real value of savings falls.

Borrowers may gain from inflation if they repay loans with money that is worth less in real terms. This is especially true when loans have fixed nominal interest rates.

Lenders may lose if inflation is higher than expected because the money they are repaid has lower purchasing power.

However, if lenders expect inflation, they may charge higher interest rates to compensate. This is why unexpected inflation is particularly important. It creates arbitrary gains and losses because people made decisions based on inflation expectations that turned out to be wrong.

Inflation and unemployment trade-offs

In some cases, reducing inflation can create short-term trade-offs with unemployment and output.

If inflation is caused by excessive aggregate demand, the government or central bank may use contractionary policy to reduce spending. Higher interest rates, lower government spending or higher taxes can shift aggregate demand left.

This may reduce inflationary pressure, but it can also reduce real output and increase unemployment in the short run.

If inflation is caused by cost-push factors, the trade-off can be even harder. Reducing aggregate demand may lower inflation, but it may also deepen the fall in output caused by the supply shock.

This is why policymakers need to identify the cause of inflation before choosing a response.

Policy responses to inflation

Governments and central banks can use several policies to reduce inflation.

Contractionary monetary policy involves increasing interest rates or reducing money supply growth. Higher interest rates make borrowing more expensive and saving more attractive. This tends to reduce consumption and investment, shifting aggregate demand left. Lower aggregate demand can reduce demand-pull inflation.

Contractionary fiscal policy involves reducing government spending, increasing taxes, or both. This also reduces aggregate demand. It may reduce inflationary pressure, but it can be politically difficult and may reduce economic growth in the short run.

Supply-side policies aim to increase productive capacity or reduce production costs. These may include investment in education, infrastructure, training, technology, competition policy or labour market reforms. If successful, supply-side policies shift long-run aggregate supply right, allowing the economy to produce more without the same inflationary pressure.

However, supply-side policies often take time and may not solve immediate inflation.

You can compare these responses in monetary policy, fiscal policy and supply-side policies.

IB exam relevance and common mistakes

Inflation is highly exam-relevant because it appears in definitions, diagrams, policy questions and evaluation.

A strong answer should define inflation as a sustained increase in the general price level. It should identify the cause, use the correct AD/AS diagram, explain the effect on real output and the price level, and evaluate policy responses.

A common mistake is saying inflation means “everything gets more expensive.” Inflation refers to the average price level, not every individual price. Some prices may rise faster than others, and some may even fall.

Another mistake is confusing inflation with a fall in purchasing power. Inflation causes purchasing power to fall if nominal income does not rise at the same rate, but the definition of inflation itself is about the general price level.

Students also sometimes confuse demand-pull and cost-push inflation. Demand-pull inflation is caused by rising aggregate demand and is shown by AD shifting right. Cost-push inflation is caused by rising production costs and is shown by SRAS shifting left.

A further mistake is assuming inflation is always bad. Low and stable inflation may be manageable and even expected in a growing economy. The bigger problems usually come from high, volatile or unexpected inflation.

Evaluation: the cause of inflation matters

The best policy response depends on the cause of inflation.

If inflation is demand-pull, contractionary monetary or fiscal policy may be effective because it directly reduces aggregate demand. However, this may also reduce growth and increase unemployment.

If inflation is cost-push, demand-side policies may be less effective and more painful. Higher interest rates can reduce demand, but they do not directly lower oil prices, food prices or imported input costs. In this case, supply-side policies may help in the long run, but they usually take time.

Inflation also affects stakeholders differently. Borrowers may benefit from unexpected inflation, while savers and fixed-income households may lose. Firms with pricing power may cope better than firms facing strong competition. Low-income households may be hit hardest if inflation is concentrated in essentials such as food, rent and energy.

This is why IB evaluation should consider the cause of inflation, the rate of inflation, whether it is expected, the time period and the effects on different stakeholders.

Conclusion

Inflation is a sustained increase in the general price level. It matters because it reduces purchasing power, creates uncertainty, affects savings and borrowing, changes firm behaviour and can damage competitiveness if it becomes too high.

Demand-pull inflation is caused by rising aggregate demand. Cost-push inflation is caused by rising production costs and falling short-run aggregate supply. Expectations can also make inflation more persistent.

The strongest IB Economics answers define inflation precisely, use AD/AS diagrams accurately, explain stakeholder effects and evaluate policy responses based on the cause of inflation and the wider macroeconomic context.

Related syllabus topics

Macroeconomic Objectives

Unit 3.3: Macroeconomic Objectives

Low and Stable Inflation

Unit 3.3: Macroeconomic Objectives

Weighted Price Index Calculation

Unit 3.3: Macroeconomic Objectives

Conflicts Between Macroeconomic Objectives

Unit 3.3: Macroeconomic Objectives

Variations in Economic Activity: Aggregate Demand and Aggregate Supply

Unit 3.2: Variations in Economic Activity: Aggregate Demand and Aggregate Supply

Shifts of the AD Curve

Unit 3.2: Variations in Economic Activity: Aggregate Demand and Aggregate Supply

Determinants and Shifts of SRAS

Unit 3.2: Variations in Economic Activity: Aggregate Demand and Aggregate Supply